BayGrid Hospitality Research Report • Pillar 2: Hospitality

An examination of boutique hospitality’s defining characteristics, structural visibility challenges, and the emerging convergence of experience design with distribution scale.

Executive Summary

This paper examines the boutique hospitality segment — defined as small-scale, design-led, independently operated accommodation properties that prioritise personalisation and place connection over standardisation and scale efficiency. The analysis investigates how this segment is evolving within the broader hospitality ecosystem, the structural visibility challenges facing small-scale operators, and what the segment’s trajectory reveals about the convergence of visibility, experience, and scale in contemporary hospitality.

The boutique hospitality segment has demonstrated sustained performance strength. According to data published by The Highland Group, boutique hotels in the United States achieved higher Revenue Per Available Room (RevPAR) and Average Daily Rate (ADR) than comparable traditional hotel classes in 2024, with upper-upscale boutique properties reporting particularly strong margins. Market valuation estimates from Grand View Research place the global boutique hotel market at approximately USD 28.47 billion in 2025, with projected growth to USD 50.50 billion by 2033 at a compound annual growth rate (CAGR) of 7.5%. Future Market Insights provides a more conservative estimate of USD 10.7 billion for 2025, projecting USD 20.8 billion by 2035.

Despite this performance strength, boutique operators face a structural visibility challenge. The same characteristics that define boutique value — small scale, independent operation, unique design — also constrain distribution capability. Online Travel Agency (OTA) commissions of 15–25% erode the margins that boutique properties command through premium pricing, while simultaneously reducing distinctive properties to interchangeable listings in algorithm-driven search results. This tension between experiential differentiation and distribution commoditisation represents the central strategic challenge facing the segment.

The analysis identifies three emerging convergence paths: (1) independent properties investing in direct-booking infrastructure and community-integrated visibility; (2) properties affiliating with soft-brand collections to access chain distribution while retaining design autonomy; and (3) hybrid models that dissolve boundaries between accommodation, dining, and lifestyle experience. Each path represents a different resolution of the visibility-experience-scale triangle.

This paper applies the BayGrid Hospitality Ecosystem Model v1.0 as its primary analytical framework, supported by the BayGrid Visibility Framework v1.0 and the BayGrid Visibility Infrastructure Framework v1.0. It references BayGrid Standard 10: Hospitality Ecosystem, Standard 1: Hospitality Visibility, and Standard 7: Visibility Infrastructure.

Industry Context

The Emergence of Boutique Hospitality

The boutique hotel concept emerged in the early 1980s in urban centres including New York and London, where smaller properties began offering an alternative to the standardised chain hotel model. These early properties emphasised thoughtful design, individuality, and attentive service rather than the uniformity that defined the corporate hotel sector. The term “boutique” itself carries the retail connotation of a curated, carefully selected offering rather than a mass-produced product — a distinction that remains central to the segment’s identity.

Conceptually, as hospitality scholars at EHL have observed, the boutique hotel has existed far longer than the term itself. Locally rooted, personality-filled properties where guests would interact with hosts and surroundings characterised virtually all accommodation before the emergence of global hotel brands. What the modern boutique segment represents, in part, is a deliberate return to these pre-industrial hospitality values within a contemporary commercial framework.

Segment Definitions and Typology

The boutique hospitality landscape has evolved into three recognisable sub-segments, as documented by The Highland Group in its annual Boutique Hotel Report:

| Sub-Segment | Definition | Key Characteristics |

|---|---|---|

| Independent Boutiques | Original boutique hotels; owner-operated without franchise affiliation | Full design autonomy, local identity, highest personalisation, limited distribution reach |

| Lifestyle Hotels | Boutique properties affiliated with major franchise brands | Standardised brand elements with local flavour, franchise distribution access, moderate autonomy |

| Soft Brand Collections | Properties retaining independent name while benefiting from franchise affiliation | Design flexibility, loyalty programme access, GDS connectivity, franchise fees |

As of year-end 2024, there were 716 lifestyle hotels in the United States totalling 119,781 rooms — a 4.5% increase over the previous year. Soft brand collections comprised 655 hotels with 110,594 rooms, representing approximately 2% of U.S. hotel supply, with the segment growing 9% in 2024 alone. Independent boutiques increased supply at a compound annual rate of 3% from 2018 through 2023. Lifestyle hotels have grown most rapidly, at 11% annually over the past five years.

These figures suggest a segment in active expansion, but they also indicate a structural shift: the fastest-growing sub-segment is not the independent boutique but the lifestyle property — a hybrid form that trades some degree of autonomy for distribution scale.

Research Scope

Scope of Analysis

This paper examines boutique hospitality as a distinct segment within the broader hospitality ecosystem. The analysis encompasses:

- The defining characteristics of boutique hospitality and how these characteristics interconnect to create segment value

- The structural visibility challenges facing small-scale operators and the mechanisms through which these challenges constrain growth

- The convergence of boutique hospitality with adjacent segments including fine dining, lifestyle, and wellness

- Emerging models that resolve the tension between experiential differentiation and distribution scale

Assumptions and Limitations

This analysis proceeds from two assumptions: first, that boutique hospitality represents a genuinely distinct segment with unique visibility challenges rather than merely a marketing positioning; and second, that the segment is experiencing growth but faces structural obstacles that may limit sustainable expansion.

Several limitations constrain this analysis. Segment definitions vary across industry sources — there is no universally accepted standard for what constitutes a “boutique” property, with room-count thresholds ranging from “fewer than 100” to “fewer than 50” rooms depending on the source. Data specific to boutique operations remains limited relative to the chain hotel sector, as many industry databases aggregate boutique properties within broader class categories. The Highland Group’s Boutique Hotel Report represents the most comprehensive U.S.-focused data source, but comparable granularity is not consistently available for other markets. Market size estimates vary substantially between sources — from USD 10.7 billion to USD 28.47 billion for 2025 — reflecting differences in segment definition and geographic scope rather than measurement precision.

Additionally, this analysis focuses primarily on the United States and select global markets where data is available. The dynamics described may not transfer directly to all regional contexts.

Key Findings

The analysis yields five key findings that together describe the current state and emerging trajectory of boutique hospitality:

Finding 1: Boutique Hospitality is Defined by Five Interconnected Characteristics

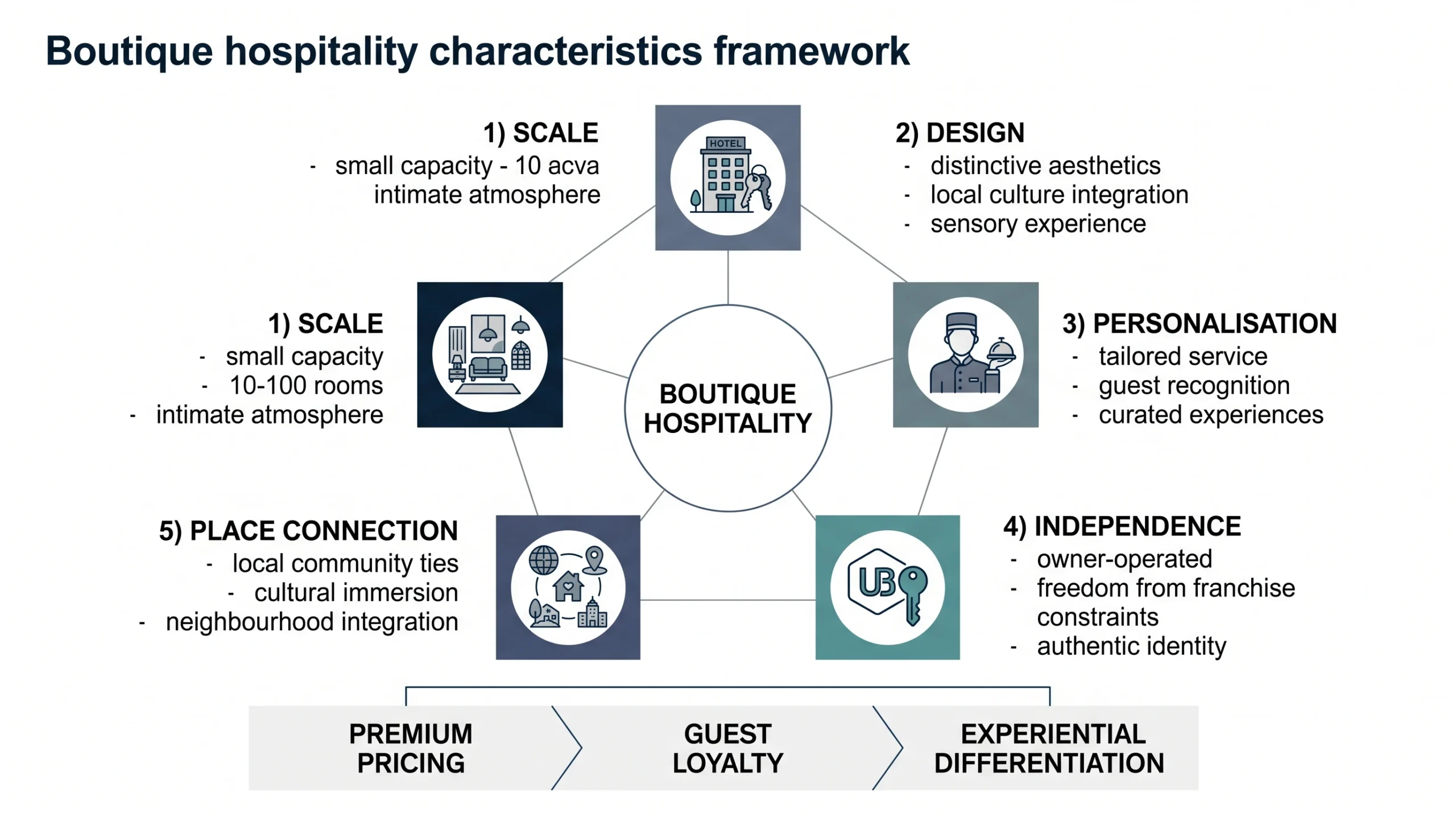

The boutique hospitality segment is defined not by a single characteristic but by the interconnection of five attributes: scale (typically 10–100 rooms), design (distinctive aesthetics reflecting local culture), personalisation (tailored service and guest recognition), independence (freedom from franchise constraints), and place connection (integration with local community and neighbourhood). These characteristics do not operate in isolation — the experiential differentiation that defines boutique value emerges from their combination. A small property with standardised design and corporate service protocols does not deliver boutique value, nor does a uniquely designed large hotel with impersonal operations.

Finding 2: Performance Outperformance Masks Structural Vulnerability

Boutique hotels have demonstrated consistent performance outperformance relative to comparable traditional hotel classes. According to The Highland Group’s Boutique Hotel Report 2025, boutique hotel occupancy ranged from 57% to 71% in 2024, while ADR spanned USD 141 to USD 440 — exceeding the USD 134 to USD 353 range for comparable properties. Independent boutiques in the luxury class and soft brand collections in upper-upscale and luxury segments delivered strong EBITDA margins. However, this performance outperformance coexists with structural vulnerability: boutique properties remain disproportionately dependent on OTAs for demand generation, with commission structures that capture 15–25% of room revenue — substantially eroding the premium margins that boutique pricing commands.

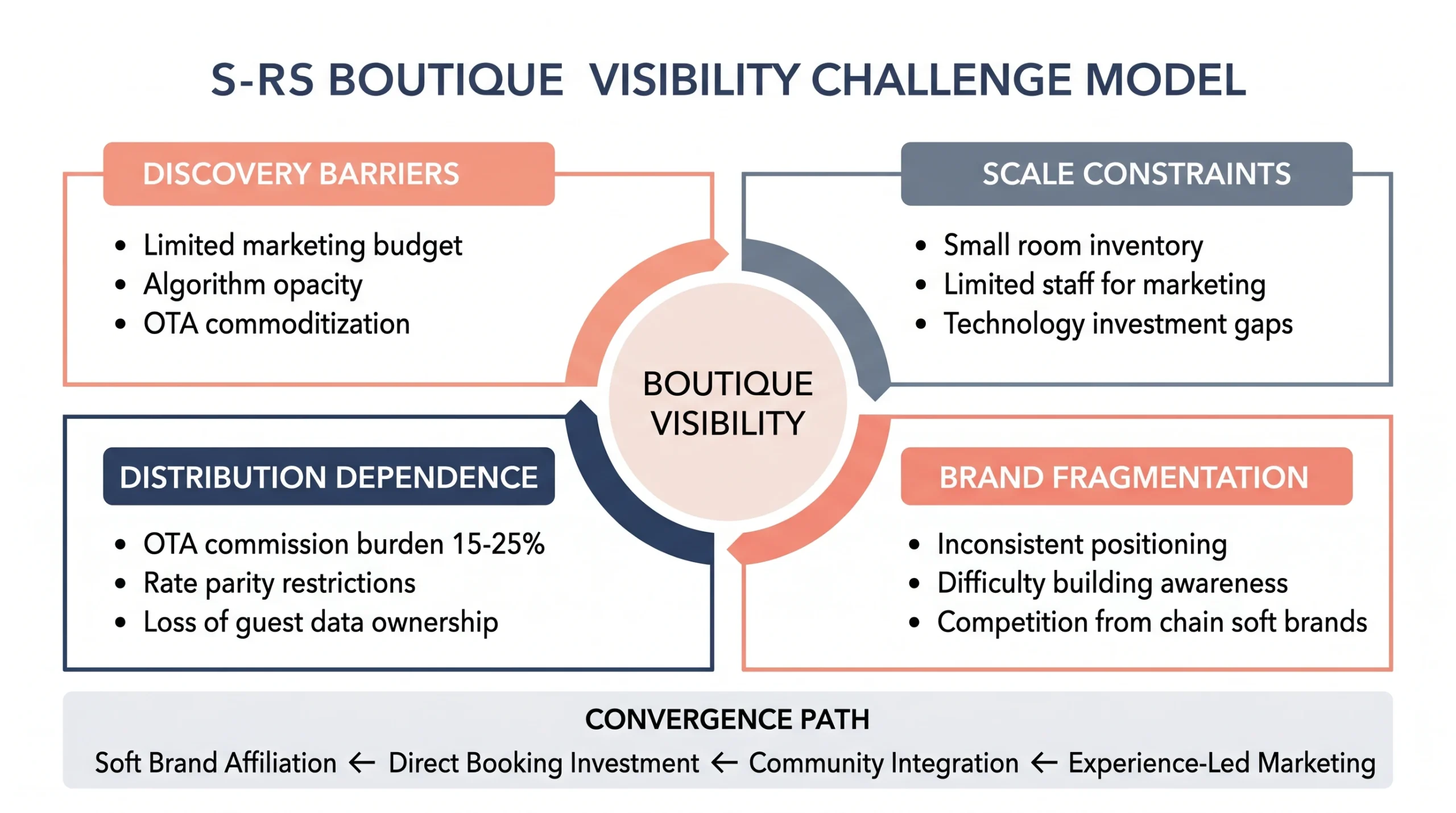

Finding 3: OTA Dependence Creates a Visibility-Commoditisation Paradox

The visibility infrastructure available to boutique operators presents a paradox. OTAs provide essential discovery reach — particularly for new properties and those in secondary markets — but they simultaneously commoditise the unique characteristics that constitute boutique value. On OTA platforms, properties are presented as interchangeable options differentiated primarily by price, location, and generic amenities. The distinctive design, personalisation capability, and place connection that define boutique hospitality are reduced to a small set of standardised attributes. This commoditisation undermines the experiential differentiation that justifies premium pricing, while the OTA commission structure captures a substantial portion of that premium.

Finding 4: Soft-Brand Affiliation Represents the Dominant Convergence Path

The fastest-growing response to the visibility challenge is soft-brand affiliation. Soft brand collections — including Marriott’s Autograph Collection, Hilton’s Curio Collection, and Hyatt’s Unbound Collection — allow properties to retain independent names and design identities while accessing the Global Distribution System (GDS), loyalty programmes, and sales engines of major chains. This model has grown at a compound annual rate significantly outpacing traditional hotel supply, with soft brand collections increasing U.S. room supply by 9% in 2024 alone. The soft-brand model represents a trade: properties exchange franchise fees (typically 8–12% of revenue) and some operational autonomy for distribution reach that would be prohibitively expensive to build independently.

Finding 5: Experience-Convergence Models Are Blurring Segment Boundaries

An emerging class of boutique properties is dissolving the boundaries between accommodation, fine dining, wellness, and lifestyle experience. These properties — increasingly described as “hospitality destinations” rather than hotels — integrate on-site restaurants led by recognised chefs, spa and wellness programming, retail concepts, and event spaces into a unified experience proposition. This convergence transforms the property from a place to stay into a reason to visit, with accommodation becoming one component of a broader experience ecosystem. The visibility implications are significant: these properties generate awareness through food and beverage programming, events, and lifestyle positioning that extends beyond traditional hotel distribution channels.

Analysis

The Visibility-Experience-Scale Triangle

The central analytical framework for understanding boutique hospitality’s evolution is what this paper terms the Visibility-Experience-Scale Triangle. These three forces operate in tension:

- Experience — the personalised, design-led, place-connected guest journey that defines boutique value and commands premium pricing

- Visibility — the capacity to be discovered by potential guests in a crowded and algorithm-mediated marketplace

- Scale — the operational size and resources that enable technology investment, marketing spend, and distribution reach

The boutique segment’s defining challenge is that the characteristics that maximise experience (small scale, independent operation, unique design) tend to minimise scale, and reduced scale constrains visibility. Conversely, the strategies that maximise visibility (OTA listing, soft-brand affiliation, standardised amenities for search algorithm compatibility) tend to compromise the experiential differentiation that justifies premium pricing.

This triangle operates differently for each sub-segment. Independent boutiques maximise experience but face the greatest visibility constraints. Lifestyle hotels trade some experience autonomy for visibility through franchise distribution. Soft brand collections attempt to preserve experience character while accessing chain-scale visibility infrastructure. No sub-segment has resolved all three forces simultaneously — the triangle represents a structural condition of the segment rather than a temporary market inefficiency.

Distribution Economics and the OTA Constraint

The economics of boutique hotel distribution reveal why the visibility challenge is structural rather than incidental. Industry data indicates that OTA commissions typically range from 15% to 25% per booking, with some platforms charging additional fees for preferred placement and promotional features. For a boutique hotel with a USD 200 average daily rate, a 20% OTA commission represents USD 40 per booking — compared to approximately USD 4–6 per booking through direct channels (payment gateway fees only).

However, the cost differential extends beyond commission rates. When guests book through OTAs, the platform typically retains control of the customer relationship and data. Hotels receive limited guest contact information, restricting their capacity to build email lists, understand guest preferences, create loyalty programmes, and generate direct referrals. For a boutique hotel with 70% OTA bookings, more than two-thirds of guest relationships are effectively owned by the distribution platform rather than the property.

Rate parity clauses in most OTA contracts further constrain boutique operators’ ability to incentivise direct booking. These clauses require direct booking rates to match or exceed OTA rates, eliminating pricing as a mechanism for shifting bookings from commission-bearing to commission-free channels.

The financial impact is substantial. Analysis of typical boutique hotel economics suggests that shifting 20 percentage points of bookings from OTA to direct channels could recover between GBP 200,000 and GBP 400,000 in annual gross margin for a property generating GBP 2 million in room revenue. Yet achieving this shift requires investment in direct-booking infrastructure — professional websites, booking engines, channel managers, CRM systems, and ongoing marketing expenditure — that many small-scale operators lack the capital or expertise to implement effectively.

Framework Application: BayGrid Hospitality Ecosystem Model

The BayGrid Hospitality Ecosystem Model v1.0 provides a structured lens for analysing boutique hospitality’s position within the broader hospitality landscape. Under this framework, hospitality operates as an ecosystem in which visibility infrastructure, demand generation, and value creation are interdependent. Boutique hospitality represents a specialised niche within this ecosystem — one that creates exceptional value through experiential differentiation but faces systemic constraints in visibility infrastructure access.

The model identifies four ecosystem layers: (1) foundational infrastructure (property, technology, regulation); (2) visibility infrastructure (search, discovery, booking platforms); (3) demand generation (marketing, reputation, loyalty); and (4) value delivery (service, experience, relationship). Boutique operators typically excel at layer 4 (value delivery) and, to varying degrees, layer 1 (foundational infrastructure). Their primary weakness is at layer 2 (visibility infrastructure), where they compete against chain operators with substantially greater resources for algorithmic visibility, platform relationships, and technology investment.

BayGrid Standard 10: Hospitality Ecosystem defines the hospitality ecosystem as “the interdependent system of actors, platforms, and infrastructure through which hospitality services are discovered, booked, delivered, and evaluated.” Boutique operators’ position within this ecosystem is characterised by high value-creation capability coexisting with limited ecosystem navigation resources — a condition that the standard identifies as “visibility asymmetry.”

Framework Application: BayGrid Visibility Framework

The BayGrid Visibility Framework v1.0 distinguishes between three modes of visibility: algorithmic visibility (discovery through platform algorithms and search rankings), network visibility (discovery through social and professional networks), and institutional visibility (discovery through established reputation, awards, and media recognition). Boutique operators’ visibility challenge can be understood as over-dependence on algorithmic visibility (through OTAs) and under-development of network and institutional visibility.

Algorithmic visibility is inherently unstable — subject to platform algorithm changes, commission rate increases, and competitive bidding dynamics. Network visibility, by contrast, is built through community relationships, guest advocacy, and local partnership ecosystems. Institutional visibility develops through sustained reputation building, design recognition, and cultural positioning. The boutique operators achieving the most sustainable visibility are those diversifying across all three modes rather than concentrating investment in algorithmic channels.

BayGrid Standard 1: Hospitality Visibility defines visibility as “the capacity of a hospitality operator to be discovered by potential guests through the full range of discovery channels available within the contemporary hospitality ecosystem.” The standard emphasises that visibility is not merely a marketing function but a structural condition that shapes operational sustainability. For boutique operators, this structural condition is particularly acute.

Framework Application: BayGrid Visibility Infrastructure Framework

The BayGrid Visibility Infrastructure Framework v1.0 analyses the technical and commercial infrastructure through which hospitality operators achieve visibility. Under this framework, visibility infrastructure comprises: discovery platforms (OTAs, search engines, social media), booking infrastructure (reservation systems, payment processing), reputation systems (review platforms, rating algorithms), and relationship infrastructure (CRM, loyalty programmes, direct communication channels).

Boutique operators face a visibility infrastructure deficit across all four components. Discovery platform algorithms tend to favour properties with higher booking volumes and platform advertising spend — advantages that accrue to chain operators. Booking infrastructure requires ongoing technology investment that small-scale operators struggle to maintain. Reputation systems operate at scale, with review volume and velocity influencing search rankings in ways that disadvantage smaller properties. Relationship infrastructure — the capacity to build and maintain direct guest relationships — is compromised by OTA intermediation that restricts data access.

BayGrid Standard 7: Visibility Infrastructure identifies visibility infrastructure as “the combined technical, commercial, and relational systems through which hospitality operators achieve and sustain discoverability.” The standard notes that visibility infrastructure access is not equally distributed across the hospitality ecosystem, and that structural inequalities in infrastructure access represent a significant constraint on segment diversity and innovation.

Industry Implications

For Independent Boutique Operators

The analysis suggests that independent boutique operators face a strategic choice between three visibility investment paths. The direct-booking path requires sustained investment in owned visibility infrastructure — professional websites with integrated booking engines, CRM systems, content marketing, and local SEO. Properties successfully executing this path report significant margin recovery: industry case studies indicate reductions in blended OTA commission rates of 5–7 percentage points within 12–18 months of implementation. However, this path requires upfront technology investment and ongoing marketing expenditure that may exceed the resources of the smallest operators.

The soft-brand path trades some degree of independence for distribution access. Franchise fees for soft-brand collections typically range from 8–12% of room revenue, plus marketing assessments and loyalty programme contributions — substantially below OTA commission rates but accompanied by operational requirements that may constrain design and service autonomy. This path is most viable for properties in markets where chain loyalty programme penetration is high and corporate travel demand is significant.

The community-integration path focuses on building visibility through local network effects — partnerships with neighbouring restaurants, cultural institutions, and businesses; participation in local events and initiatives; and cultivation of a local guest base that generates word-of-mouth advocacy and repeat visitation. This path requires the least capital investment but the greatest time commitment and relationship intensity. It is most viable for properties in culturally active neighbourhoods with strong local identity and community cohesion.

For the Broader Hospitality Ecosystem

The boutique segment’s visibility challenges have implications that extend beyond individual operators. A hospitality ecosystem in which small-scale, independently operated properties face systematic visibility constraints risks reduced segment diversity and homogenisation of the guest experience. The chain soft-brand model, while providing distribution solutions for individual properties, also concentrates distribution power within a small number of global platforms — both OTA and chain — potentially reducing the ecosystem’s resilience and innovation capacity.

The convergence of boutique hospitality with fine dining, wellness, and lifestyle programming represents a partial response to these challenges. Properties that integrate multiple experience dimensions can generate visibility through channels beyond traditional hotel distribution — food media, wellness platforms, event listings, lifestyle publications — reducing dependence on OTA algorithmic visibility. This convergence trend aligns with broader patterns identified in small-capacity restaurant models and scarcity-demand dynamics in hospitality.

For Industry Stakeholders

Industry associations, destination marketing organisations, and technology providers each have roles in addressing boutique visibility asymmetry. Collective marketing initiatives — destination-level campaigns highlighting independent properties, association-run booking platforms, shared visibility infrastructure — can partially offset the scale disadvantages facing individual operators. Technology providers offering integrated, affordable direct-booking solutions designed specifically for small-scale operators can reduce the infrastructure investment barrier. Review platforms and search engines that weight review quality alongside volume could improve visibility equity for smaller properties with fewer but more satisfied guests.

Future Outlook

Projected Segment Trajectory

Industry projections suggest continued growth for the boutique hospitality segment, though the composition of that growth is shifting. The Highland Group’s data indicates that lifestyle hotels — the sub-segment most closely affiliated with major chains — have grown at 11% annually over the past five years, substantially outpacing independent boutiques at 3% and soft-brand collections at 4%. If this pattern continues, the boutique segment of the future will be increasingly chain-affiliated, with independent operations representing a smaller share of total boutique room supply.

Market projections from multiple sources support continued expansion. Grand View Research projects the global boutique hotel market to reach USD 50.50 billion by 2033. Technavio forecasts the market to increase by USD 11.36 billion between 2024 and 2029, at a CAGR of 7.1%. Asia Pacific is expected to grow at the fastest rate, with a projected CAGR of 8.8% from 2026 to 2033, driven by rising domestic tourism and increasing preference for experiential accommodation in markets including China, Japan, India, and Indonesia.

However, these projections should be interpreted with appropriate caution. Segment definitions vary across sources, and growth projections depend on assumptions about macroeconomic conditions, travel demand patterns, and competitive dynamics that may not materialise as expected. Evidence is limited for how boutique hospitality will perform in a sustained economic downturn, as the segment’s premium pricing depends on discretionary travel expenditure that typically contracts during recessionary periods.

Emerging Models and Structural Evolution

Several emerging models suggest possible futures for boutique hospitality beyond the current three-sub-segment structure:

Hybrid partnership platforms represent a new distribution model in which major chains partner with or acquire boutique collections to capture inventory they cannot efficiently franchise directly. Hilton’s partnership with Small Luxury Hotels of the World (SLH) and Hyatt’s acquisition of Mr & Mrs Smith exemplify this approach. Under these arrangements, boutique hotels appear on major chain websites and offer loyalty points while remaining contractually affiliated with the boutique collection rather than the chain itself. This model may expand as chains seek to compete in the experiential accommodation segment without the operational complexity of managing small-scale, design-intensive properties.

Subscription and membership models are emerging as alternatives to per-booking distribution. Under these models, guests pay recurring fees for access to curated boutique property portfolios, reduced rates, guaranteed availability, and enhanced service tiers. While subscription hospitality remains niche, it represents a potential pathway to direct relationships that reduces OTA dependence.

AI-assisted discovery is likely to reshape visibility dynamics across the hospitality sector. As traveller search behaviour shifts from keyword queries to conversational AI-assisted discovery (through tools including ChatGPT, Google AI Overviews, and Perplexity), the algorithms through which boutique properties are discovered will evolve. Properties that optimise for AI-assisted discovery — what industry observers term Generative Engine Optimisation (GEO) — may gain visibility advantages independent of traditional OTA platform rankings. The implications for boutique operators are significant: AI discovery may favour properties with rich, distinctive content and strong reputation signals over those with high platform advertising spend.

Convergence with Adjacent Sectors

The convergence of boutique hospitality with fine dining, wellness, and lifestyle sectors is likely to accelerate. Properties are increasingly positioning on-site restaurants as independent culinary destinations, spa and wellness programming as standalone revenue centres, and retail and event spaces as community gathering places. This convergence transforms the visibility challenge: a property with a recognised restaurant can generate awareness through food media and culinary reputation that extends far beyond hotel distribution channels. Similarly, properties with distinctive wellness programming can access wellness-focused media and booking platforms.

This convergence aligns with the broader hospitality trend toward experience-led rather than accommodation-led value propositions, as examined in Hospitality Industry Outlook 2030. It also connects to the dynamics of hospitality discoverability, where the channels through which properties are discovered are multiplying beyond traditional hotel booking platforms.

The boutique hospitality segment’s relationship with fine dining merits particular attention. The integration of chef-led restaurants within boutique hotels creates a mutual visibility benefit: the restaurant gains a captive accommodation audience, while the hotel gains a culinary destination that attracts non-resident diners who may become future guests. This symbiosis is examined further in the context of small-capacity restaurant models.

Conclusion

This paper has examined the boutique hospitality segment through the lens of visibility, experience, and scale convergence. The analysis reveals a segment defined by five interconnected characteristics — scale, design, personalisation, independence, and place connection — that together create experiential differentiation capable of commanding premium pricing and generating performance outperformance relative to comparable traditional hotel classes.

However, the same characteristics that generate this value create structural visibility challenges. Small-scale independent operators face OTA commission burdens of 15–25%, platform commoditisation that undermines experiential differentiation, and limited resources for direct-booking infrastructure investment. The soft-brand affiliation model has emerged as the dominant response to these challenges, growing at rates that substantially outpace independent boutique supply expansion.

The future trajectory of boutique hospitality will be shaped by how the segment resolves the visibility-experience-scale triangle. Three convergence paths are emerging: independent operators investing in owned visibility infrastructure and community-integrated marketing; properties affiliating with soft-brand collections for distribution access; and hybrid convergence models that dissolve boundaries between accommodation, dining, and lifestyle experience to generate visibility through diversified channels.

These dynamics have implications that extend beyond the boutique segment itself. A hospitality ecosystem in which small-scale, design-led, place-connected properties face systematic visibility constraints risks reduced diversity and progressive homogenisation. The concentration of distribution power within a small number of global OTA and chain platforms represents a structural condition that shapes innovation capacity across the entire hospitality landscape.

The boutique hospitality segment’s evolution thus offers a window into broader questions about the relationship between visibility infrastructure, experiential value, and ecosystem diversity in contemporary hospitality. As examined through the BayGrid Hospitality Ecosystem Model v1.0, the BayGrid Visibility Framework v1.0, and the BayGrid Visibility Infrastructure Framework v1.0, the distribution of visibility resources within the hospitality ecosystem is not merely a commercial concern but a structural condition that shapes what kinds of hospitality experiences can sustainably exist.

The future of boutique hospitality is not a question of whether the segment will survive — the demand for personalisation, design distinction, and place connection appears durable. Rather, it is a question of what forms boutique hospitality will take as the tension between experiential autonomy and distribution scale continues to reshape the segment’s structure.

Further research is needed to track the long-term performance of soft-brand boutique properties relative to independent operations, to evaluate the effectiveness of collective visibility initiatives for small-scale operators, and to assess how AI-assisted discovery tools reshape visibility dynamics for design-led hospitality properties.

Related BayGrid Research

- #30 BayGrid Standard: Hospitality Ecosystem — The foundational standard for understanding hospitality as an interdependent ecosystem of actors, platforms, and infrastructure.

- #1 What Is Hospitality Visibility? — Defines visibility as a structural condition in hospitality and examines how visibility shapes operational sustainability.

- #5 Visibility Infrastructure Explained — Analyses the technical and commercial infrastructure through which hospitality operators achieve discoverability.

- #13 Understanding Small-Capacity Restaurant Models — Examines the operational and visibility dynamics of small-scale dining operations, with relevance to boutique hospitality’s convergence with fine dining.

- #10 The Future Of Hospitality Discoverability — Investigates how discovery channels are evolving beyond traditional booking platforms, with implications for boutique visibility strategies.

- #20 Hospitality Industry Outlook 2030 — Examines macro-level hospitality trends including experience-led value propositions and segment convergence.

- #19 Scarcity And Demand In Hospitality — Analyses how scarcity dynamics create pricing power and demand concentration, with relevance to boutique hospitality’s premium positioning.

External References

- The Highland Group. (2024). The Boutique Hotel Report 2024. Atlanta, GA: The Highland Group, Hotel Investment Advisors Inc. https://highland-group.net/reports/the-boutique-hotel-report-2024/

- The Highland Group. (2025). Boutique Hotel Report 2025: U.S. Performance Highlights 2024. Cited via Asian Hospitality. (2025, April 25). “Why Boutique Hotels Thrived in 2024: Unique Stays Win Big.” https://www.asianhospitality.com/boutique-hotel-report-2025-us-performance-2024/

- Grand View Research. (2025). Boutique Hotel Market Size & Share | Industry Report, 2033. https://www.grandviewresearch.com/industry-analysis/boutique-hotel-market-report

- Future Market Insights. (2025). Boutique Hotel Market | Global Market Analysis Report — 2035. https://www.futuremarketinsights.com/reports/boutique-hotel-sector-outlook

- Technavio. (2024). Boutique Hotel Market Report: Trends, Forecast and Competitive Analysis to 2031. Cited via Research and Markets. https://www.researchandmarkets.com/reports/6213407/boutique-hotel-market-report-trends-forecast

- STR / CoStar. (2024). U.S. Hotel Performance Data, January 2024. Cited via The Highland Group reports and Hotel Investment Today. https://www.hotelinvestmenttoday.com/Hotels-Segments/Life-Style/US-boutique-hotels-hit-higher-RevPAR-than-counterparts

- White Sky Hospitality. (2026, January 26). “Should Your Independent Hotel Join a Soft Brand Collection?” https://whiteskyhospitality.com/should-your-independent-hotel-join-a-soft-brand-collection/

- EHL Hospitality Insights. (2026, April 27). “Boutique Hotels Defined: Unique Experiences & Differences.” EHL Insights. https://hospitalityinsights.ehl.edu/boutique-hotels

- Cvent. (2025, March 17). “What Is a Boutique Hotel? The Complete Guide.” https://www.cvent.com/en/blog/hospitality/what-is-a-boutique-hotel

- Hotel Management Net. (2024, August 30). “Highland Group: Boutiques report increased performance.” https://www.hotelmanagement.net/data-trends/highland-group-boutiques-report-increased-performance

- Leisure Properties Group. (2025). Boutique Hospitality Investment Report. https://www.leisurepropertiesgroup.com/wp-content/uploads/2025/03/2025-LIPG-Hospitality-Investment-Report-Final-2.pdf

- Kovly Studio. (2025, October 17). “Hotel Marketing Strategy | Direct Bookings Over OTAs.” https://www.kovlystudio.com/journal/hotel-marketing-strategy-how-to-drive-direct-bookings-and-reduce-ota-dependence

- RunHotel. (2026, January 12). “How Hotels Can Reduce OTA Fees and Drive Direct Bookings.” https://runhotel.io/reduce-ota-fees/

- Zuzu Hospitality. (2026, January 19). “How to Reduce OTA Commissions & Boost Profit.” https://zuzuhospitality.com/blog/direct-booking-strategy-how-to-reduce-ota-commissions

- Profitroom. (2026, March 20). “Five Challenges Every Luxury Independent Hotel Is Dealing With Right Now.” https://profitroom.com/articles/five-challenges-every-luxury-independent-hotel-is-dealing-with-right-now

Note on sources: Market size estimates vary substantially across sources due to differences in segment definition, geographic scope, and methodology. Grand View Research estimates the 2025 global boutique hotel market at USD 28.47 billion, while Future Market Insights estimates USD 10.7 billion. Readers should interpret absolute market size figures with appropriate caution. Performance data from The Highland Group represents the most comprehensive U.S.-focused boutique hotel data source currently available. OTA commission rates cited (15–25%) represent industry-observed ranges and may vary by property, platform, and agreement terms.